As retirement approaches, many investors face the challenge of balancing income needs, tax efficiency, and legacy planning. This case study highlights how we helped a 77-year-old retired business owner restructure her portfolio, address significant tax concerns, and create a plan that provides income for nearly eight decades — while protecting her heirs.

Client Profile

Client came to us for financial guidance as she neared her late seventies. Client had built a sizeable investment account

and owned many individual stock positions. She also owned an annuity with John Hancock in her individual name. This

annuity had significant taxable gains that would cause income tax implications on her withdrawals.

Age: 77

Background: Retired entrepreneur and lifelong self-directed investor

Portfolio:

Trust Account – approx. $840,000

Roth Account – approx. $17,000

Variable Annuity with John Hancock

Cost basis: $225,000

Contract Value: $968,734

Unrealized gains: ~$740,000

Personal Situation: Recently experienced health challenges, with family living out of town. Needed personalized guidance after years of navigating investments independently.

Her primary goal was clear: continue growing her wealth aggressively, while ensuring an efficient plan for withdrawals and estate transfer.

The Challenge

Although a significant amount of growth was realized in these accounts, no one had ever coordinated with the client to understand the tax implications or the estate planning considerations she needed to be exploring.

Despite her investment success, two major issues stood out:

Tax Exposure – Withdrawals from her annuity would be taxed as ordinary income. This meant her heirs would face significant tax liabilities.

Lack of Diversification – Her portfolio was highly concentrated in individual securities without an investment policy strategy, creating unnecessary risk.

Additionally, outdated account titling and limited estate planning documents risked complicating wealth transfer.

Our Process

Portfolio Review – We identified nearly $282,000 in unrealized capital gains and a heavily concentrated stock allocation.

Portfolio Review – We identified nearly $282,000 in unrealized capital gains and a heavily concentrated stock allocation.Estate Planning Coordination – We worked with attorneys to restructure her trust and ensure her wishes were clearly documented.

Risk Management – Developed a phased diversification plan to gradually rebalance her holdings while managing capital gains exposure.

Withdrawal Planning – Sought a strategy that would allow for efficient income without front-loading taxes.

The Strategy

We knew the client needed to live off of some of these assets and that she also wanted them to grow

aggressively for her use and for her to pass on to her heirs. This could have caused an issue with taxes if we paid

the funds needed from her current annuity. The annuity represented nearly half of her invested assets and was

not only one of her least performing investments but also would cause her to incur the largest amount in taxes.

The breakthrough came with a tax-free annuity exchange into a new contract that allowed for:

Tax-efficient withdrawals: Gains and principal paid out proportionally, reducing the immediate tax burden.

Longevity planning: By naming her 11-year-old grandchild as the annuitant, the contract extended income payments for up to 79 years, creating a lasting stream of benefits for future generations.

Additional guarantees: The annuity included lifetime income protection, even if the account value reached zero.

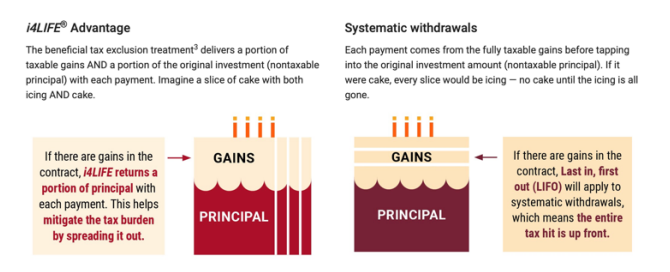

The solution we presented to the client was a tax free exchange to a new annuity company. This new company

had a Private Letter Ruling from the IRS that allowed them to pay out part of a distribution as a return of basis

and part as gains. Essentially allowing her to spread out the gains over all of her withdrawals instead of having to

incur all of her gains before reaching into her basis. As shown below, gains and principal are paid out with each

withdrawal.

The second benefit our client enjoyed with making this transition was that the annuity company would allow her

to change the annuitant to someone other than herself. An annuitant is an individual whose age is used to set

the life expectancy length of the contract benefits. Usually, an annuitant and an owner are the same individuals.

In this case, making someone else the annuitant allowed the client to create a longer income payout from the

annuity.

Results & Impact

When we were initially introduced to this client, her major pain points were that she had little to no support in a

relationship with an advisory team and she had significant capital gains across nearly all of her investments. We were able to provide her with multiple resources for market analysis, execution of trades, and investment strategy for a longer-term view. We were also able to reduce the overall risk of her portfolio. We were able to implement strategies to provide significant tax savings to the client and her heirs. We were also able to create an income stream that could last nearly eight decades.

Reduced tax exposure on gains, preserving more wealth for her heirs.

Created an income stream lasting nearly eight decades.

Established clear estate planning structures, ensuring her wishes are honored.

Lowered portfolio risk through gradual diversification.

Gave her the confidence of having a trusted advisory team after years of managing investments alone.

Key Lessons

This case illustrates the power of combining investment strategy, tax planning, and estate coordination:

A diversified portfolio reduces unnecessary risk.

Properly structured annuities can create both tax savings and legacy income.

Estate planning is essential for protecting heirs and reducing complications.

Proactive financial advice can turn complex challenges into opportunities.

By rethinking her portfolio structure and leveraging innovative annuity strategies, our client secured her financial stability while creating a lasting income stream for her heirs. What began as a challenge of concentrated risk and heavy tax exposure became a plan designed to benefit her family for generations to come.